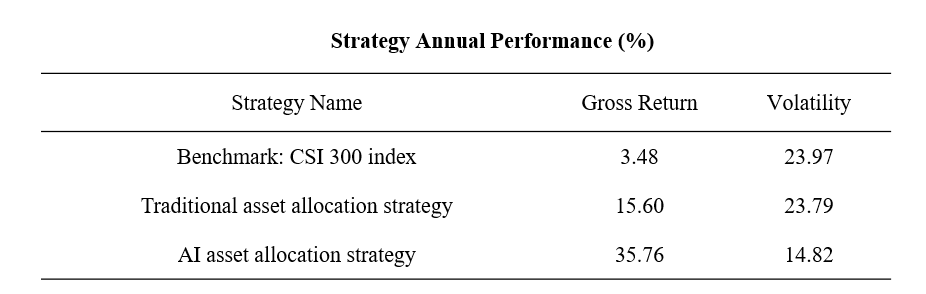

吴辉航,魏行空和张晓燕(2019)研究发现,与市场组合投资和基于传统算法的资产配置策略相比,基于人工智能高级算法的资产配置策略能取得更好的业绩。

Wu, Wei and Zhang (2019) find that Fintech can empower institutional investor efficiency. Compared with traditional strategy, AI asset allocation strategy generates better performance.

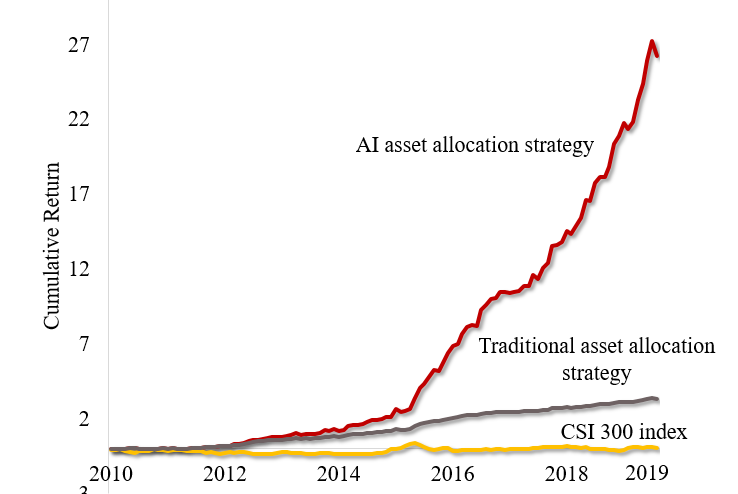

2010年1月-2019年8月回测结果(Backtest Performance: 2010.01-2019.08)

【2】投资于人工智能基础算法策略能得到3.30元

【3】投资于人工智能高级算法策略能得到26.27元

How much you can get from 2010 to 2019, if you invest $1 in different ways:

【1】For CSI 300 index, you can get $1.18

【2】For Traditional strategy, you can get $3.30

【3】For AI asset allocation strategy, you can get $26.27

Wu, Wei and Zhang (2019) find that Fintech can empower institutional investor efficiency. Compared with traditional strategy, AI asset allocation strategy generates better performance.

2010年1月-2019年8月回测结果(Backtest Performance: 2010.01-2019.08)

如果在2010年投资1元钱,到了2019年:

【2】投资于人工智能基础算法策略能得到3.30元

【3】投资于人工智能高级算法策略能得到26.27元

How much you can get from 2010 to 2019, if you invest $1 in different ways:

【1】For CSI 300 index, you can get $1.18

【2】For Traditional strategy, you can get $3.30

【3】For AI asset allocation strategy, you can get $26.27

* 研究结果来自工作论文《机器学习视角下中国股票资产收益率可预测性研究》(吴辉航,魏行空,张晓燕,2019)

* 论文曾在第二届中国金融学术与政策论坛(2019)、2019年中国金融科技学术年会进行展示,并获得第二届中国金融学与政策论坛(2019)优秀论文奖

* 作者邮箱:wuhh@pbcsf.tsinghua.edu.cn (吴辉航), weixk@pbcsf.tsinghua.edu.cn (魏行空), zhangxiaoyan@pbcsf.tsinghua.edu.cn (张晓燕).

* “Are Stock Returns Predictable in China? A Machine Learning Approach” (in Chinese) by Huihang Wu, Xingkong Wei and Xiaoyan Zhang, Dec. 2019, Submitted. Winner of the 2019 CFTRC Best Paper Award.

* This paper benefitted from discussions with conference participants at China International Forum on Finance and Policy (CIFFP 2019) and China Fintech Research Conference (CFTRC 2019).

* E-mail addresses: wuhh@pbcsf.tsinghua.edu.cn (H. Wu), weixk@pbcsf.tsinghua.edu.cn (W. Wei), zhangxiaoyan@pbcsf.tsinghua.edu.cn (X. Zhang).